Reverse home loans decrease the quantity of equity you have in your residence. As with any type of large monetary choice, it is very important to evaluate the advantages and disadvantages to ensure this is the right alternative for you Offering your house will unlock your equity and also provide you with capital that might surpass your expectations if your home value has actually valued. However if your residence has actually valued in value, you could market, scale down, as well as save or invest the added cash. The funding and also interest are paid off just when you sell your residence, completely move away, or pass away. However the loan provider does not determine to whom the property possession will be approved.

- With non-HECM reverse home loans, you can shed vital customer defenses, as well as you will not be assured the consistent needs supplied by the FHA.

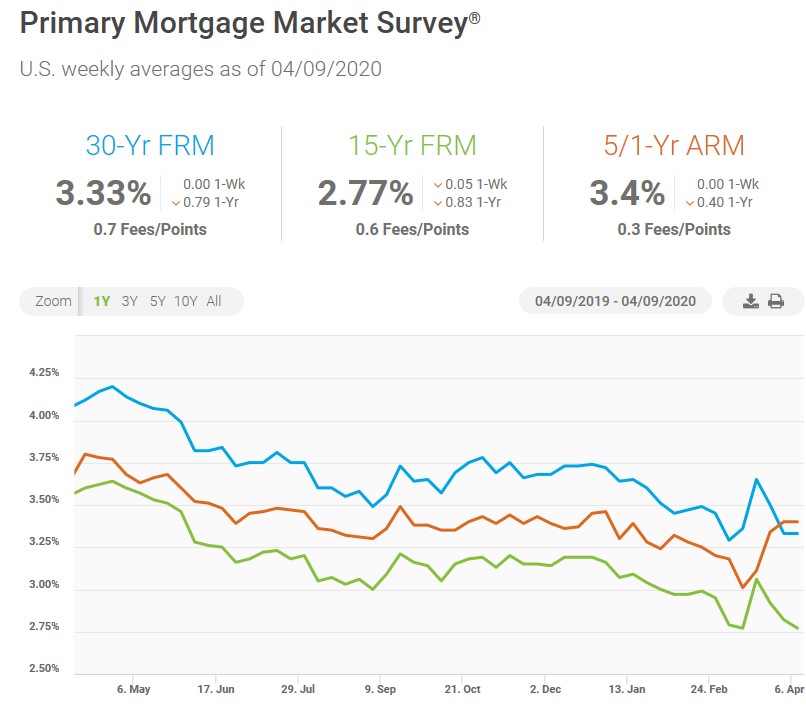

- Similar to any type of major monetary decision, you ought to evaluate the benefits and drawbacks of obtaining a reverse mortgage and determine if it is best for you.

- The decision to wfg contact take a reverse home mortgage should constantly be considered as a specific approach considering long-term viability.

- As long as your car loan is a non-recourse funding, you'll never pay even more on the lending than the worth of your house.

- The lending as well as interest are paid off just when you offer your house, permanently relocate away, or pass away.

- Remember that, depending upon the type of reverse mortgage you choose, there may be limits positioned on exactly how you can utilize the money.

. Financings used by some banks and also mortgage business can be made use of for any kind of purpose. A lot of need no settlement for as long as you stay in your house. If you are seeking to use the reverse for purchase program as well as wanting to handle extra commitments and responsibility, the expectation is that you are an excellent supervisor of your funds presently prior to you take on a new home. That does not mean that you must take the entire amount for which you qualify though. Champion is right in that they can not give you any type of details regarding a lending that the customer on the finance never ever provided then written authorization to talk about with you if you are not likewise on the funding.

Reverse Home Loan Prices

Unlike a normal mortgage in which the house owner pays to the lending institution, with a reverse home mortgage, the lending institution pays the home owner. Proprietary reverse mortgages are exclusive fundings that aren't backed by a federal government company. Lenders set their own eligibility demands, rates, fees, terms and also underwriting procedure. For a reverse home mortgage to be a viable financial choice, existing mortgage balances typically need to be low enough to be repaid with the reverse home loan earnings. However, debtors do have the choice of paying down their existing mortgage wesley tour balance to receive a HECM reverse home loan.

Where To Get A Reverse Mortgage

Consumers can choose to get their cash in a number of different means, consisting of a lump sum, fixed month-to-month settlements, a line of credit or a mix of routine payments and line of credit. You could be able to obtain even more cash with a proprietary reverse http://andresbtuk407.jigsy.com/entries/general/exactly-how-the-fed-s-price-choices-affect-home-mortgage-prices mortgage. A HECM counselor or a loan provider can aid you contrast these sorts of car loans side by side, to see what you'll get-- as well as what it sets you back. Only the lump sum reverse mortgage, which provides you every one of the profits at the same time when your financing closes, has a set rate of interest. The various other five alternatives have flexible rates of interest, which makes feeling given that you're obtaining cash over many years, not all at once, and rate of interest are always changing. Variable-rate reverse mortgages are connected to the London Interbank Offered Price.

If a private or company is pressing you to authorize an agreement, for example, it's likely a red flag. Reducing expenses-- Cutting discretionary expenses can aid you stay in your residence long-lasting. If you need help with a necessary bill, think about getting in touch with a neighborhood help company, which may have the ability to aid with gas repayments, utility bills as well as required home fixings. Origination cost-- To process your HECM funding, loan providers charge the greater of $2,500 or 2 percent of the first $200,000 of your residence's worth, plus 1 percent of the amount over $200,000. " Commonly, the house owner or beneficiaries are not responsible for any type of expenses if your house is cost much less than the quantity owed," adds Sullivan. Just like any various other kind of home mortgage, you possess the house in a reverse home mortgage scenario.

You can make monthly settlements, you can pay quarterly, bi-monthly, semi-annually or all at once. In addition, the line of credit scores expands in accessibility on the unused funds in time. This implies that the longer you have funds readily available on the line, the even more cash will be readily available to borrow later should you require them. If you never ever draw the cash, you never accumulate any rate of interest on the funds and you, or your successors do not require to repay them.

Heirs Taking Care Of Reverse Mortgages Commonly Face Roadblocks

Originally, you have a "right of rescission," which means you can cancel the lending as well as have your finance costs refunded if you alert your loan provider in composing within 3 days of closing on the funding. After that, you'll require to either pay off the lending or refinance it if you no longer desire a reverse home loan. Prior to getting a reverse home mortgage, double-check that you have a means for your estate or life insurance policy to repay the financial obligation if maintaining the home in the family is an essential priority. There are means to navigate this, such as deeding the home to the older partner as well as leaving the non-qualifying companion off the reverse mortgage, but this approach might create issues later. As a whole, if both partners don't get approved for an FHA-insured reverse mortgage, it could make sense to wait until both satisfy the demand. FHA reverse mortgage loans are non-recourse, so you can't owe greater than the existing value of the building.

Rate of interest, service fees, and mortgage insurance will all be analyzed as well as contributed to the finance balance. With many reverse home loans, you can never ever owe more than your home is worth. In a regular "forward" home mortgage, the debtor obtains a lump sum of cash from the lender, and then makes regular monthly payments in the direction of paying back the cash, including interest. There are some advantages to a reverse home mortgage if it is prepared well.

Other than the potential for rip-offs targeting the senior, reverse home loans have some genuine threats. In spite of recent reforms, there are still scenarios when a widow or widower can shed the home upon their spouse's death. " If I have a reverse mortgage, will my youngsters or successors have the ability to keep my home after I pass away?" Accessed Nov. 23, 2021. Relocating into a long-term care facility or a retirement home counts as no longer utilizing your residence as a key home. If you remain in an assisted living facility or various other care facility for 12 successive months, your finance becomes due. Learn whether the reverse home loan you are considering is federally-insured.